Line of Credit and Credit Score Health in Canada

A Line of Credit (LOC) can be a useful tool in Canada, but it can also turn into stubborn debt if you treat it like extra income. It lets you borrow up to a limit, repay, and borrow again. You pay interest only on what you use, and the rate is often variable.

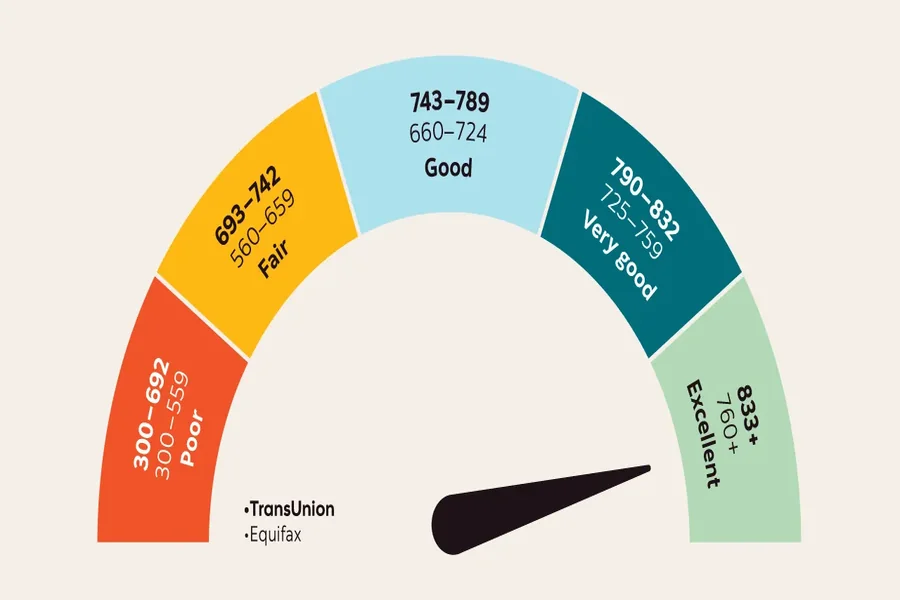

Credit scores react to patterns. They reward on-time payments and sensible use of available credit. They also look at things like the age of your accounts and how often you apply for new credit.

Many people first see a LOC through a pre-approved offer, or as a lower interest option than carrying a credit card balance. Some lenders connect it closely to everyday banking. The personal LOC offered by Innovation Credit Union is an example of a setup where funds can be accessed easily alongside a chequing account.

To protect your score, focus on three things you can control: balance ratios, utilization habits, and payment timing.

How a LOC Affects Your Credit File

Most personal LOCs are revolving credit, like credit cards. Revolving accounts matter because they influence credit utilization. When you open a new LOC, your score can dip for a short time because accepting it usually involves a hard check, and a new account can lower the average age of your credit. Good management helps the score recover.

Balance Ratios and Why 30 Percent Matters

A balance ratio is what you owe compared with your limit. If your limit is $10,000 and you owe $2,500, that account is at 25 percent. Scores also consider your total utilization across revolving accounts, so your cards and LOCs work together.

A practical target is to keep revolving utilization under 30 percent. Lower is often better, especially before you apply for a mortgage or other major loan. A LOC can help your ratio if it raises your available credit and you keep the balance low. It can hurt if you borrow a large amount and keep it there for months. Maintaining a versatile business line of credit provides a powerful safety net for your company’s cash flow while simultaneously strengthening your overall credit profile through responsible use.

Utilization Habits That Keep You Out of Trouble

Use it with a plan. A LOC works best for a short-term gap, a project with uncertain costs, or consolidating higher-interest debt. It works poorly as a permanent backup for overspending. If you borrow, decide how you will pay it back and by when.

Avoid living near the limit. Using a high percentage of your limit signals risk. If you need long-term financing for a large amount, a loan with a set payoff schedule may fit better.

Pay down principal on purpose. Many lines of credit set the minimum payment around the monthly interest. Paying only interest can keep the account in good standing, but it can leave the balance almost unchanged. Choose a fixed monthly amount that reduces the principal, even if the lender does not require it.

Watch your total revolving balances. A modest LOC balance can still push you over 30 percent if you also carry credit card balances.

Making a LOC Work for Debt Payoff

If you use a LOC to pay off higher-interest debt, treat it like a one-way move. For example, you might transfer a $3,000 credit card balance to your LOC to lower interest. That can help, but only if you stop building the card balance again.

Pick a fixed payment that would clear the balance in a reasonable time, like 12 to 24 months, and stick with it. If your minimum payment is interest only, set up an extra payment so the principal actually drops. When cash is tight, paying extra even once or twice a year can still help because it reduces daily interest charges.

Timing Payments Right

Paying on time is non-negotiable. Late payments can hurt your score quickly, and the impact can linger. If you worry about forgetting, set up automatic payments for at least the minimum.

But timing is not only about the due date. Most lenders report your balance to the credit bureaus monthly. If your balance is high when it is reported, your utilization can look high, even if you plan to pay it down right after.

You cannot always control the reporting date, but you can keep balances from spiking by paying sooner and more often. Two simple habits help:

- Make a payment soon after a large withdrawal.

- If you use the LOC regularly, make smaller payments more than once a month.

This also saves money. Interest on a LOC is typically calculated daily, so earlier payments reduce interest costs.

Choosing the Right Kind of Line of Credit

In Canada, you may see secured and unsecured options. A secured line uses an asset as collateral, often a home in the case of a home equity LOC. Because the lender has collateral, secured lines may offer lower rates and higher limits. Unsecured lines rely more on your creditworthiness and income, and may have higher rates.

For your credit score, the type matters less than your behaviour. For your budget, it matters because rates are often variable. If a rate increase would strain your cash flow, borrow less and pay down faster.

Pre-Approved Offers and Quick Decision Checks

A pre-approved offer can be convenient, but accepting it may still trigger a hard credit check. Before you accept, check three things. First, whether you have a clear need or a clear emergency use case. Second, whether you understand the minimum payment rule, fees, and rate type. Third, whether you are likely to keep utilization low instead of turning the new limit into new debt.

The Bottom Line

A LOC is flexible, but your credit score likes steady habits. Keep utilization reasonable, pay on time, and pay down principal consistently. That is what turns a LOC into a help instead of a headache.